50/30/20 Rule Explained: How to Manage Your Money Better

The 50/30/20 rule is a simple budgeting method that suggests using 50% of your take-home pay for needs, 30% for wants, and 20% for savings and extra debt payments, making it one of the easiest ways to manage money better without tracking every dollar in a complicated spreadsheet.

If you have ever felt like budgeting was too detailed, too restrictive, or too hard to maintain, the 50/30/20 rule is probably popular for a reason. It gives you a clear structure without forcing you to build a full line-by-line budget from scratch. The Consumer Financial Protection Bureau says that making and sticking to a budget is a key step toward getting a handle on debt and working toward savings goals, and this rule gives people a straightforward framework for doing exactly that.

The reason this rule still matters is simple. Most people do not need a perfect budget first. They need a usable one. And in 2026, that matters even more because household spending is still heavily concentrated in a few major categories. The Bureau of Labor Statistics reported that average US household spending in 2024 was $78,535, with housing taking up 33.4% and transportation 17.0%, meaning those two categories alone accounted for over half of total spending. That is exactly why a simple percentage-based budget can be useful. It helps you see whether your biggest expenses are leaving enough room for everything else.

This guide explains what the 50/30/20 rule is, how it works, what counts as needs and wants, where debt payments fit in, when the rule works well, when it does not, and how to adapt it if your real-life expenses do not match the textbook percentages. If you want a budgeting system that feels realistic and easy to apply in the US, this is one of the best places to start.

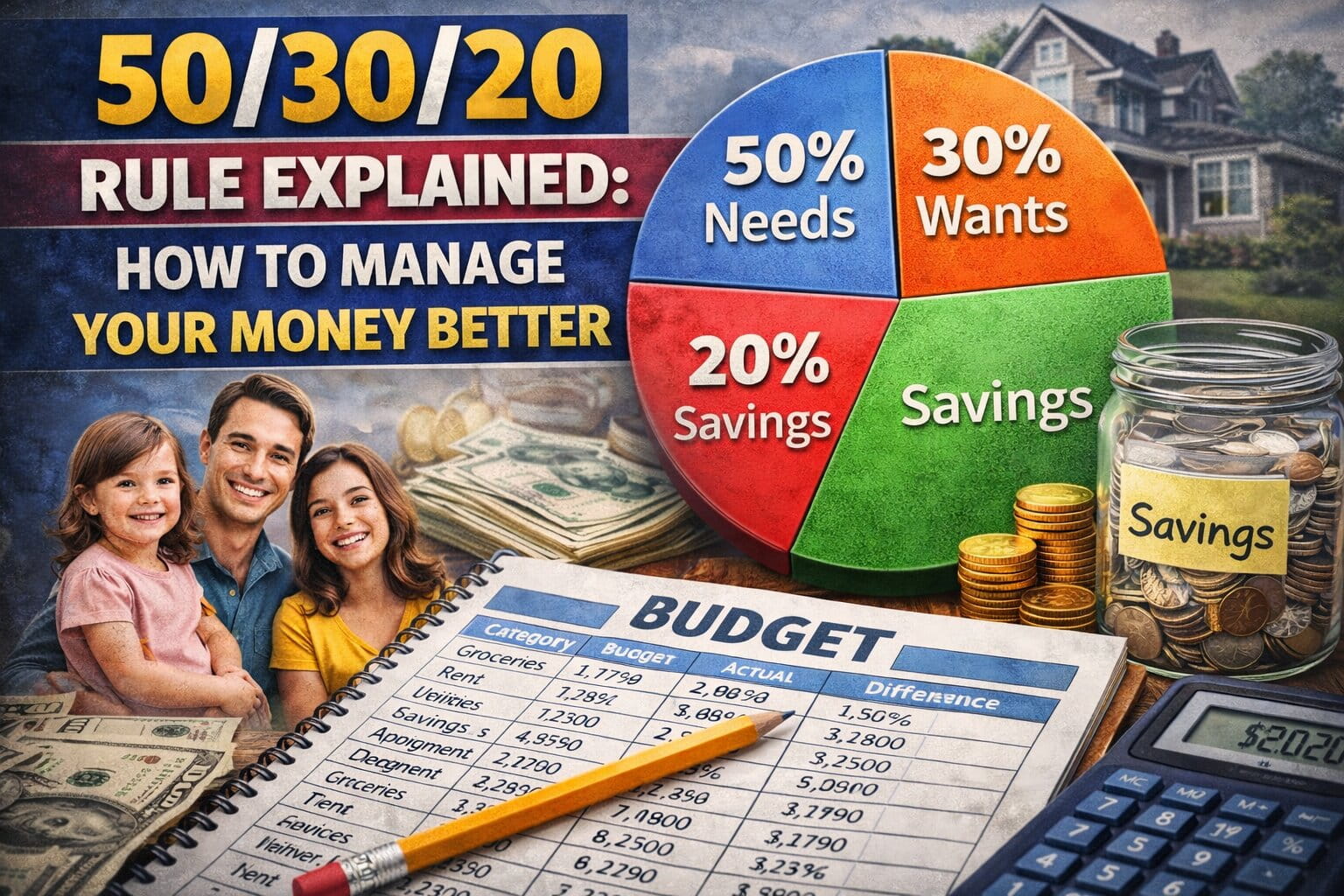

What is the 50/30/20 rule?

The 50/30/20 rule is a budgeting framework that divides your after-tax income into three broad categories. Fifty percent goes to needs, 30% goes to wants, and 20% goes to savings and debt repayment. NerdWallet describes it this way in both its budget calculator and budget worksheet guidance, and CFPB materials also reference the 50-30-20 structure in budget learning resources.

What makes this rule so appealing is that it simplifies budgeting. Instead of tracking 20 or 30 separate categories, you work with three big buckets. That gives you flexibility while still creating limits. You can spend differently inside each bucket from month to month, as long as the overall balance stays close to the plan. That flexibility is an inference from how the rule is structured.

In plain English, the rule asks three questions. Are your essential expenses staying near half of your take-home pay? Are your lifestyle purchases staying near 30%? And are you directing at least 20% toward savings or paying down debt beyond minimums? If the answer is yes, your money plan is probably in decent shape. If the answer is no, the rule helps you see where the pressure is.

Why the 50/30/20 rule works for so many people

The biggest strength of the 50/30/20 rule is simplicity. A budget only helps if you keep using it, and many people abandon detailed systems because they take too much time or feel too rigid. CFPB says budgeting starts with getting a realistic picture of how much money is coming in and where it is going, and this rule gives people a fast way to do that without getting lost in tiny categories.

Another reason it works is that it balances present life with future goals. It does not tell you to spend everything on bills and cut out all fun. It also does not tell you to ignore savings. The structure leaves room for essentials, room for enjoyment, and room for long-term progress. That balanced design is one reason the rule has stayed popular.

It also works well as a diagnostic tool. If your needs are taking up 65% or 70% of your take-home pay, the issue may not be that you are bad with money. The issue may be that your fixed expenses are too high for your income. If your wants are consistently swallowing 40% or more, the rule shows where your budget is losing discipline. If your savings rate is near zero, it makes the gap impossible to ignore. That practical use is an inference from the ratio-based design of the method.

What counts as “needs” in the 50/30/20 rule?

Needs are the expenses you must cover to function and stay current on essential obligations. Consumer.gov defines bills and expenses in examples such as rent, electricity, water, telephone service, food, and gas, and those are the types of items that normally fall into the “needs” category.

In most households, needs include housing, utilities, groceries, transportation required for work or daily life, insurance, minimum debt payments, childcare needed to work, and basic medical costs. Housing and transportation are especially important here because BLS data shows they already consume a huge share of average US household spending.

The key idea is necessity, not comfort level. A basic phone plan may be a need. The most expensive unlimited plan may not be. A reasonable car payment for commuting may be a need. A luxury vehicle upgrade is not. Groceries are a need. Daily restaurant delivery usually is not. That distinction is an inference based on the standard budgeting definition of essential versus discretionary spending.

What counts as “wants”?

Wants are the things you enjoy but could reduce, delay, or live without if you had to. They usually include dining out, entertainment, streaming subscriptions, travel, hobbies, upgraded shopping, convenience purchases, and lifestyle extras. NerdWallet’s 50/30/20 guidance frames wants as the nonessential portion of your take-home pay.

This is the category that causes the most confusion because many purchases sit in the gray area. Internet service might feel essential. A premium internet tier may be a want. Clothing can be a need, but impulse shopping is not. Transportation is a need, but expensive add-ons may not be. The rule still works, though, because it is meant to guide decisions, not create courtroom arguments over every purchase. That interpretive point is an inference from how broad-budget methods function.

If you are unsure whether something is a need or a want, ask one question: if money got tight this month, would this expense still have to happen? If the answer is no, it probably belongs in wants.

What goes into the 20% category?

The 20% bucket usually covers savings and debt repayment beyond minimum required payments. NerdWallet’s 50/30/20 explanations state that this part of the budget goes toward savings and paying off debt. Its savings goal guidance also says the 20% portion can be used for savings and debt repayment beyond minimums.

That means this bucket can include emergency fund contributions, retirement contributions, sinking funds, investing, and extra payments on high-interest debt. Minimum debt payments generally belong in the needs category because they are required. Extra debt payoff belongs in the 20% category because it improves your financial position rather than simply keeping you current. That distinction is a standard practical interpretation of the rule reflected in personal finance guidance.

This is also where the rule becomes powerful. It does not just tell you to avoid overspending. It requires you to build financial progress into the budget itself. CFPB says budgeting is connected to saving goals, and this 20% bucket is the part that turns a spending plan into a money-growth plan.

How to calculate your 50/30/20 budget

The first step is to use your take-home pay, not your gross salary. NerdWallet’s calculator says to use monthly after-tax income and even add back payroll deductions for health insurance, 401(k) contributions, and other automatic savings when appropriate for its calculator logic. For most readers, the simplest version is to start with the amount that actually hits your bank account each month.

Then multiply that number by the three percentages:

- 50% for needs

- 30% for wants

- 20% for savings and extra debt payoff

For example, if your monthly take-home pay is $4,000, your starting targets would be:

- $2,000 for needs

- $1,200 for wants

- $800 for savings and extra debt payments

That math follows directly from the 50/30/20 framework.

After that, compare the targets with your real spending. NerdWallet recommends looking at your last one to three months of spending and stacking it up against the budget framework. That part matters because the rule is most useful when it shows the gap between your ideal plan and your current reality.

A real-world example of the 50/30/20 rule

Let’s say someone brings home $5,000 a month after taxes. Under the 50/30/20 rule, they would aim for:

- $2,500 for needs

- $1,500 for wants

- $1,000 for savings and extra debt payoff

Now imagine their actual spending looks like this: rent and utilities $1,800, groceries $500, gas and insurance $450, minimum debt payments $250, streaming and subscriptions $80, dining out $300, shopping and fun $550, travel sinking fund $150, emergency savings $300, and extra credit card payoff $620.

This budget is close to the framework because essentials remain around the 50% mark, wants stay near the 30% range, and savings plus extra debt payoff combine into the 20% bucket. The usefulness of the example is illustrative, but the allocation method follows the rule directly.

The point is not to hit every number with perfect precision. The point is to create proportions that keep your money balanced.

How the 50/30/20 rule helps you manage money better

The rule helps you manage money better because it creates boundaries without overcomplicating your life. CFPB says that until you understand where your money is going, it is difficult to know whether you will have enough left over to save. The 50/30/20 method solves that by showing how much room should exist for essentials, lifestyle spending, and future goals.

It also improves decision-making. Once you know your needs bucket is already overloaded, you stop pretending the budget problem is just coffee or small treats. If your wants bucket is too large, you know where cuts are most likely to matter. If your savings bucket is too small, the rule forces you to face whether your current spending actually supports your goals. That practical effect is an inference from the structure of the rule.

Another benefit is that it works well with automation. The 20% bucket can be moved automatically to savings, retirement, or extra debt payoff right after payday. CFPB’s emergency savings guide emphasizes creating a system for consistent contributions, and this rule gives that system a percentage target.

When the 50/30/20 rule works best

The 50/30/20 rule works best for people with steady income, moderate fixed costs, and a desire for a simple system. It is especially useful for beginners because it provides structure without demanding a full zero-based budget from day one. That assessment is an inference from the broad and simple design of the framework.

It also works well for people who already have basic control over spending but want a better overall plan. If you are not deeply in crisis and mostly need a way to organize your money more clearly, this rule is often a strong fit. CFPB’s budgeting guidance supports starting with a realistic picture of income and expenses, which matches how this method is meant to be used.

When the 50/30/20 rule may not work well

The 50/30/20 rule does not fit every household. In high-cost areas, many people cannot keep needs at 50% of take-home pay even when they are spending responsibly. BLS data showing that housing and transportation alone already account for over half of average household spending helps explain why fixed costs can overwhelm traditional budgeting ratios.

It may also be too loose for people who need more control. If you repeatedly overspend, ignore account balances, or are trying to aggressively pay off debt, a more detailed system like zero-based budgeting may work better. That is an inference based on the fact that broad ratios create flexibility but less category-level control.

It can also feel discouraging if your income is low and essentials are already consuming most of your paycheck. In that case, the rule is still useful as a diagnostic tool, but it may not work as a strict target right away.

How to adapt the 50/30/20 rule if your costs are too high

One of the smartest ways to use the 50/30/20 rule is as a starting point, not a rigid law. NerdWallet explicitly says the percentages can be changed to fit your financial needs at a given moment. If saving or debt payoff is the priority, you can shrink wants and increase the savings bucket. If fixed costs are unusually high, you may need a temporary adjustment while you work on bigger structural changes.

For example, some households may operate closer to 60/20/20, 60/30/10, or 55/25/20 for a while. The important thing is not whether the ratio looks perfect on paper. The important thing is whether you know where your money is going and whether the budget is helping you move forward. That flexible use is consistent with the rule’s practical application.

If your needs are too high, the long-term fix usually involves the biggest categories, not tiny ones. Since housing and transportation consume such a large share of average spending, those areas often deserve the first serious review.

Common mistakes people make with the 50/30/20 rule

The first mistake is using gross income instead of take-home pay. The rule is generally built around after-tax income, so using pre-tax salary can distort the whole budget.

The second mistake is mislabeling wants as needs. That makes the budget look tighter than it really is and hides lifestyle inflation inside the essentials bucket. This is a practical interpretation issue that comes up with all broad budgeting systems.

The third mistake is ignoring the 20% bucket or treating it as optional. If the savings and extra debt category is consistently empty, the budget may look stable on the surface while still failing to build long-term security. CFPB connects budgeting directly to savings goals, which is why this category matters so much.

The fourth mistake is trying to make the rule fit perfectly in a clearly imperfect situation. If your rent is too high or your income is unstable, the answer may be adaptation, not self-blame.

50/30/20 rule vs zero-based budgeting

The 50/30/20 rule and zero-based budgeting solve different problems. The 50/30/20 rule gives you a big-picture framework. Zero-based budgeting gives every dollar a specific assignment. NerdWallet explains zero-based budgeting as a method where income minus expenses equals zero because all money is allocated intentionally.

If you want a simple, low-maintenance budget, 50/30/20 is usually easier. If you need stronger control or are paying off debt aggressively, zero-based budgeting may be better. That comparison is an inference based on the differing levels of detail in the two systems.

50/30/20 rule vs pay-yourself-first

Pay-yourself-first focuses on moving money to savings before spending it elsewhere. FDIC educational material defines this as saving and setting aside money before spending.

The 50/30/20 rule includes that logic inside the 20% bucket, but it also gives you guidance for needs and wants. So if your main problem is simply that savings never happens, pay-yourself-first may be enough. If you need a fuller view of your overall money balance, 50/30/20 is stronger. That distinction is an inference from the scope of each method.

A simple step-by-step way to start using the 50/30/20 rule

Start by pulling your last one to three months of bank and credit card statements. NerdWallet recommends this because it helps you compare your real spending to the target budget.

Next, total your take-home pay for one month. Then calculate the three targets:

- 50% needs

- 30% wants

- 20% savings and extra debt payoff

After that, sort your spending into the three buckets. Do not worry about perfection on the first pass. The goal is to get a realistic picture. CFPB emphasizes realism in budgeting, and Consumer.gov similarly starts with listing bills, expenses, and income.

Then pick one change. Maybe you reduce wants by $150 and move it to savings. Maybe you realize your needs are too high and start reviewing housing, car, or subscription costs. Maybe you automate your 20% bucket. Small adjustments are often easier to keep than dramatic changes.

Final takeaway

The 50/30/20 rule is one of the easiest budgeting methods to understand because it tells you to use 50% of take-home pay for needs, 30% for wants, and 20% for savings and extra debt payments. It works well because it is simple, flexible, and practical enough for real life, especially for people who want to manage money better without building an overly detailed budget.

It is not perfect for every household, especially in places where fixed costs are unusually high, but it remains one of the best starting points for anyone who wants a clearer, healthier relationship with money. Use it as a framework, compare it with your real spending, and adjust it when necessary. A budget does not need to be perfect to be useful. It just needs to help you make better money decisions consistently.

Related Articles

Emergency Fund: How Much Should You Save in the US?

Apr 17, 2026How to Create a Monthly Budget (Step-by-Step for Beginners)

Apr 17, 2026Best Budgeting Methods That Actually Work in 2026

Apr 17, 2026How to Save Money Fast on a Low Income (US Guide)

Apr 17, 2026Secured vs Unsecured Credit Cards: Which Is Better?

Apr 17, 2026Get Updates

Subscribe to get the latest articles delivered to your inbox.